Trade, Monopoly, and the Fight We Can’t Let Trump Define Tariffs and trade are not side issues, but a central front in the battle against monopoly power—and for self-government.

0

President Donald Trump is drastically shrinking the workforce and mission of the Consumer Financial Protection Bureau, eviscerating an agency created after the Great Recession with the goal of protecting Americans from fraud, abuse and deceptive practices.

The plan, which is being challenged by an employee union, is the latest step in an extraordinary reshaping of the federal government. Conservatives and businesses have often chafed at the agency’s oversight and investigations, and Elon Musk made it a top target of his Department of Government Efficiency.

Roughly 1,500 employees are slated to be cut, leaving around 200 people, according to an administration official who wasn’t authorized to disclose the figure publicly and spoke on condition of anonymity. Fox Business first reported the number of layoffs.

Employees started receiving layoff notices on Thursday. Their access to agency systems, including email, ends on Friday evening.

“The Consumer Financial Protection Bureau identified your position being eliminated, and your employment is subject to termination by reduction-in-force (RIF) procedures,” the emails said.

The Trump administration’s plans have been the subject of a legal battle. A federal judge initially blocked what she described as “a hurried effort to dismantle and disable the agency.”

However, an appeals court said Friday that layoff notices could be sent “to employees whom defendants have determined, after a particularized assessment, to be unnecessary to the performance of defendants’ statutory duties.”

On Thursday, the National Treasury Employees Union asked a federal judge to step in by arguing that officials were violating the order.

“It is unfathomable that cutting the Bureau’s staff by 90 percent in just 24 hours, with no notice to people to prepare for that elimination, would not ‘interfere with the performance’ of its statutory duties, to say nothing of the implausibility of the defendants having made a ‘particularized assessment’ of each employee’s role in the three-and-a-half business days since the court of appeals imposed that requirement,” the union wrote.

Mark Paoletta, the chief legal officer for the agency, sent a message to employees on Wednesday describing the CFPB’s reduced mission.

“To focus on tangible harms to consumers, the Bureau will shift resources away from enforcement and supervision that can be done by the States,” he wrote.

Problems with mortgages will be the top priority, while issues involving medical debt, student loans and digital payments will receive less attention, according to Paoletta.

The change in focus could benefit Musk’s efforts to offer financial services through X, his social media company. He has long wanted to allow users to make peer-to-peer payments using his platform, and he announced in January that X would be working with Visa.

Such services will now be a lower priority for the CFPB.

Sen. Elizabeth Warren, a Massachusetts Democrat who helped create the CFPB, said in a statement that Trump was preventing the agency from doing “its job of helping Americans who get scammed by big banks and giant corporations.”

She described his plans as “yet another assault on consumers and our democracy by this lawless administration, and we will fight back with everything we’ve got.”

The CFPB was formed in 2010, two years after the financial crisis and subprime mortgage-lending scandal. Officials said that it has obtained nearly $20 billion in financial relief for U.S. consumers since its founding in the form of canceled debts, compensation and reduced loans.

Slower growth, rising inflation, and an increasing likelihood of a U.S. recession are among the takeaways from a new survey of economists conducted byThe Wall Street Journal. The survey of 64 economists sees a 45% probability of a recession this year, though several respondents noted that shifts in the White House’s tariff agenda make their forecasts “unusually uncertain.” Meanwhile, the International Monetary Fund is set torelease forecastsnext week showing an expected slowdown in global economic growth.

Trump’s Trade Tariffs: A Monopoly Power Grab

Donald Trump’s trade policy, centered on imposing steep tariffs—10-20% on all imports and up to 60% on Chinese goods—promises to reshape the U.S. economy. Presented as a defense of American workers, these tariffs are more likely to enrich corporate monopolies, raise consumer prices, and disrupt global supply chains, with devastating consequences for the working class.

Tariffs are a tax on imports, historically used to protect domestic industries or raise revenue. Trump’s plan, however, is unprecedented in scale, targeting $4 trillion in annual imports. Economists warn this could spike inflation by 5-10%, with consumer prices for essentials like food, clothing, and electronics rising sharply. The Tax Foundation estimates a $300 billion annual tax hike, disproportionately hitting low- and middle-income households. Retaliatory tariffs from trading partners, as seen in 2018 when China targeted U.S. agricultural exports, could further harm American farmers and exporters.

The real beneficiaries? Large corporations. Tariffs shield dominant firms from foreign competition, allowing them to raise prices without fear of losing market share. Historical examples abound: in 2018, Trump’s steel tariffs enabled U.S. Steel to jack up prices, boosting profits while downstream industries like auto manufacturing faced higher costs and job cuts. Economists call this “rent-seeking”—when firms leverage government policy to extract unearned profits. Today’s economy, marked by extreme corporate consolidation (90% of industries are controlled by a handful of firms), amplifies this risk. From Big Tech to Big Pharma, monopolies already exploit their power to overcharge consumers. Tariffs would hand them a blank check.

Trump’s rhetoric about bringing manufacturing jobs back ignores reality. Modern supply chains are global, and tariffs disrupt them, raising costs for U.S. manufacturers reliant on imported components. Studies show his 2018 tariffs destroyed more jobs than they created, with 175,000 losses tied to higher costs and retaliation. Automation, not trade, has driven most manufacturing job losses—robots don’t return with tariffs. Meanwhile, offshoring continues: U.S. firms invested $1.2 trillion abroad in 2022, undeterred by Trump’s policies.

The economic fallout could be catastrophic. The Peterson Institute projects a 7% GDP drop by 2029 under Trump’s plan, akin to a self-inflicted Great Recession. Developing nations, reliant on U.S. markets, face economic collapse, potentially triggering migration surges—ironic given Trump’s border rhetoric. Allies like Canada and Mexico, hit by tariffs, may retaliate, straining diplomatic ties. China, though targeted, has diversified its trade, reducing its vulnerability.

Corporate lobbying fuels this agenda. In 2018, firms secured tariff exemptions through political connections, not merit. Today, industries like steel and tech are poised to cash in again, with campaign contributions already flowing to Trump-aligned PACs. Antitrust enforcement, critical to curbing monopoly power, is absent from his platform, signaling open season for price gouging.

Progressives must counter with bold alternatives: strengthen antitrust laws, tax excess profits, and invest in green manufacturing to create jobs without inflationary tariffs. Trade policy should prioritize workers, not corporate giants. Trump’s tariffs risk entrenching monopoly power and impoverishing millions—a betrayal of the very workers he claims to champion.

The number of Americans filing new applications for unemployment benefits fell to a two-month low last week, suggesting labor market conditions remained stable in April, though uncertainty around tariffs is making businesses hesitant to boost hiring.

President Donald Trump's import duties are squeezing the housing market, with other data on Thursday showing single-family housing starts plunging to an eight-month low in March, which underscored economists' expectations that economic growth likely ground to a halt in the first quarter.

Federal Reserve Chair Jerome Powell on Wednesday acknowledged the heightened uncertainty and signs the economy appeared to have slowed in the first quarter.

"The labor market remains resilient," said Michael Pearce, deputy chief U.S. economist at Oxford Economics. "We are most concerned about small businesses, which are responsible for a large share of total employment and job creation and are less able to withstand gyrations and uncertainty in tariff policy."

Initial claims for state unemployment benefits dropped 9,000 to a seasonally adjusted 215,000 for the week ended April 12, the lowest level since February, the Labor Department said.

Economists polled by Reuters had forecast 225,000 claims for the latest week. There are still no signs that mass firings of federal government workers have significantly impacted the labor market.

Initial jobless claims and JOLTS firings

The data suggested companies had not yet responded with layoffs to Trump's April 2 "Liberation Day" tariff announcement, but the White House's trade policy has constantly shifted, which economists said made it difficult for businesses to plan ahead.

Trump has slapped duties on virtually all foreign goods, igniting a trade war with China, the biggest source of U.S. imports. The hit from tariffs, together with the drag from tightening financial conditions, could still come.

Businesses appear to be cutting hours rather than laying off workers. A separate report from the Philadelphia Fed showed the average workweek at factories in the mid-Atlantic region contracted sharply in April and a measure of future manufacturing employment dropped to the lowest level since 2016.

The tariffs, viewed by Trump as a tool to raise revenue to offset his promised tax cuts and to revive a long-declining U.S. industrial base, have stoked fears of high inflation and stagnation in economic growth.

Low layoffs have anchored the labor market. With business sentiment in the doldrums, economists are bracing for a rise in unemployment in the coming months. The claims data covered the period during which the government surveyed businesses for the nonfarm payrolls component of April's employment report.

Claims declined during the March and April survey weeks, suggesting a steady pace of job gains this month. The economy added 228,000 jobs in March while the unemployment rate rose to 4.2% from 4.1% in February.

Next week's data on the number of people receiving benefits after an initial week of aid, a proxy for hiring, could shed more light on the labor market's fortunes in April.

The so-called continuing claims increased 41,000 to a seasonally adjusted 1.885 million during the week ending April 5, the claims report showed, indicating some laid-off workers were finding it difficult to land new opportunities.

Stocks on Wall Street fell as tariffs continued to weigh on investor sentiment. The dollar was steady against a basket of currencies. U.S. Treasury yields were mixed.

Continuing claims and jobs confidence

CHAOTIC TARIFF POLICY

A third report from the Commerce Department's Census Bureau showed single-family housing starts, which account for the bulk of homebuilding, dropped 14.2% to a seasonally adjusted annual rate of 940,000 units in March, the lowest level since July.

They decreased 9.7% year-on-year. Weak homebuilding added to economists' expectations that gross domestic product growth slowed to below a 0.5% annualized rate in the first quarter, with greater odds for a contraction.

A surge in imports as businesses front-loaded goods to avoid tariffs accounts for some of the anticipated stall in growth. The economy grew at a 2.4% pace in the fourth quarter.

A National Association of Home Builders survey on Wednesday showed sentiment among single-family homebuilders remained depressed in April. The NAHB said the impact of import duties was already being felt with "the majority of builders reporting cost increases on building materials due to tariffs."

It said suppliers have, on average, raised their prices by 6.3%, meaning that builders estimated a typical cost effect from recent tariff actions at $10,900 per home. These increased costs have overshadowed a recent moderation in mortgage rates, driven by concerns over the economy's outlook.

There is also little incentive for builders to continue breaking ground on housing projects, with new housing inventory at levels last seen in late 2007.

"Even before all of the tariff news, housing demand was tepid and new home inventories were bloated," said Stephen Stanley, chief U.S. economist at Santander U.S. Capital Markets. "Thus, it would be far from shocking to see housing starts decline. Add to that the uncertainty regarding the economic outlook created by the chaotic tariff policies."

Permits for future construction of single-family housing fell 2.0% to a rate of 978,000 units in March.

Starts for housing projects with five units or more were unchanged at a rate of 371,000 units.

Overall housing starts tumbled 11.4% to a rate of 1.324 million units. Economists polled by Reuters had forecast housing starts falling to a rate of 1.420 million units.

Multi-family building permits jumped 10.1% to a rate of 445,000 units. That lifted overall building permits by 1.6% to a pace of 1.482 million units last month.

Housing starts and building permits

The number of single-family houses approved for construction that were yet to be started surged 6.5% to 148,000 units, the highest level in nearly three years.

The completion rate for that housing segment rose 0.9% to 1.029 million. The inventory of single-family housing under construction dropped 1.6% to a rate of 632,000 units, the lowest level since February 2021.

"A significant decline in new residential construction projects looks likely to add to the broader headwinds facing the economy over the next quarter or two," said Oliver Allen, senior U.S. economist at Pantheon Macroeconomics.

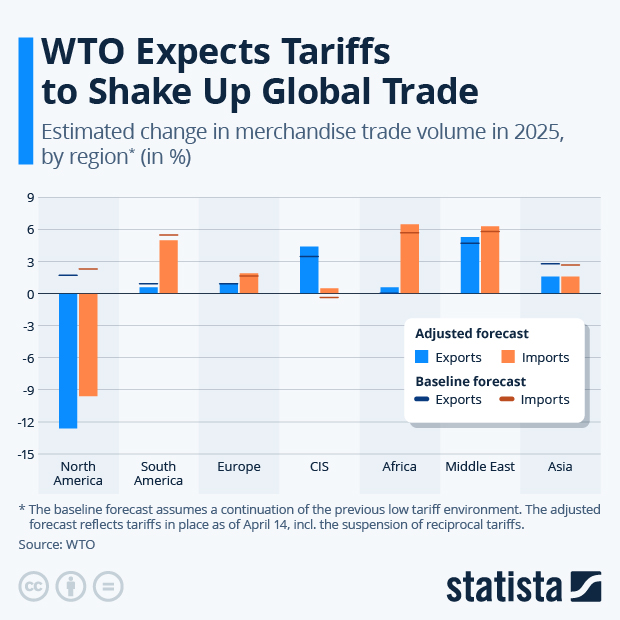

The world’s economic resilience is once again being tested. Like a pot that’s been bubbling for a long while and is now boiling over, trade tensions have triggered very high levels of uncertainty. The result? Ships at sea, not knowing which port to sail to, market volatility, and postponed investment decisions. The longer the uncertainty persists, the higher the cost. And as the giants face off, smaller countries are caught in the crosscurrents.

Raising the curtain on the much-anticipatedInternational Monetary FundSpring Meetings today, Managing DirectorKristalina Georgievahighlights the challenges facing the world economy and what must be done to turn this moment of challenge into one of opportunity. Because with cool heads, clear vision, and strong will, times of change can be times of renewal.

Trump's tariffs are ostensibly designed to help American businesses. Yet even some "proudly made in the USA" companies rely on imported materials, meaning that they're getting hit by duties to the point that they're pausing hiring and investment projects. Take Fresh Press Farms, which grows olives, nuts and seeds locally, presses them domestically, and bottles them in the US. The caveat? Its glass bottles come from China (145% tariff). The aluminum for its American-made bottles comes from Canada (25% tariff). The levies are "incredibly painful," the company's CEO said.

Trump’s Trade Tariffs: A Monopoly Power Grab

Donald Trump’s trade policy, centered on imposing steep tariffs—10-20% on all imports and up to 60% on Chinese goods—promises to reshape the U.S. economy. Presented as a defense of American workers, these tariffs are more likely to enrich corporate monopolies, raise consumer prices, and disrupt global supply chains, with devastating consequences for the working class.

Tariffs are a tax on imports, historically used to protect domestic industries or raise revenue. Trump’s plan, however, is unprecedented in scale, targeting $4 trillion in annual imports. Economists warn this could spike inflation by 5-10%, with consumer prices for essentials like food, clothing, and electronics rising sharply. The Tax Foundation estimates a $300 billion annual tax hike, disproportionately hitting low- and middle-income households. Retaliatory tariffs from trading partners, as seen in 2018 when China targeted U.S. agricultural exports, could further harm American farmers and exporters.

The real beneficiaries? Large corporations. Tariffs shield dominant firms from foreign competition, allowing them to raise prices without fear of losing market share. Historical examples abound: in 2018, Trump’s steel tariffs enabled U.S. Steel to jack up prices, boosting profits while downstream industries like auto manufacturing faced higher costs and job cuts. Economists call this “rent-seeking”—when firms leverage government policy to extract unearned profits. Today’s economy, marked by extreme corporate consolidation (90% of industries are controlled by a handful of firms), amplifies this risk. From Big Tech to Big Pharma, monopolies already exploit their power to overcharge consumers. Tariffs would hand them a blank check.

Trump’s rhetoric about bringing manufacturing jobs back ignores reality. Modern supply chains are global, and tariffs disrupt them, raising costs for U.S. manufacturers reliant on imported components. Studies show his 2018 tariffs destroyed more jobs than they created, with 175,000 losses tied to higher costs and retaliation. Automation, not trade, has driven most manufacturing job losses—robots don’t return with tariffs. Meanwhile, offshoring continues: U.S. firms invested $1.2 trillion abroad in 2022, undeterred by Trump’s policies.

The economic fallout could be catastrophic. The Peterson Institute projects a 7% GDP drop by 2029 under Trump’s plan, akin to a self-inflicted Great Recession. Developing nations, reliant on U.S. markets, face economic collapse, potentially triggering migration surges—ironic given Trump’s border rhetoric. Allies like Canada and Mexico, hit by tariffs, may retaliate, straining diplomatic ties. China, though targeted, has diversified its trade, reducing its vulnerability.

Corporate lobbying fuels this agenda. In 2018, firms secured tariff exemptions through political connections, not merit. Today, industries like steel and tech are poised to cash in again, with campaign contributions already flowing to Trump-aligned PACs. Antitrust enforcement, critical to curbing monopoly power, is absent from his platform, signaling open season for price gouging.

Progressives must counter with bold alternatives: strengthen antitrust laws, tax excess profits, and invest in green manufacturing to create jobs without inflationary tariffs. Trade policy should prioritize workers, not corporate giants. Trump’s tariffs risk entrenching monopoly power and impoverishing millions—a betrayal of the very workers he claims to champion.

.webp)

.webp)

.webp)